Natural Money is an interest-free demurrage currency. It features a holding fee on currency and a maximum interest rate of zero on money and loans. The Natural Money currency is an accounting unit only, as the holding fee, which may range from 0.5% to 1% per month, makes the currency unattractive to hold. Therefore, the currency will not circulate, nor will someone invest in it. Cash, bank deposits, bonds, stocks, real estate, and other investments aren’t currency and therefore not subject to the holding fee. Not paying the holding fee and the curtailment of credit, and thereby inflation, caused by the maximum interest rate, can make lending at negative interest rates attractive.

Natural Money features a separation between regular banking, also known as commercial banking, which involves lending and borrowing, and investment banking, also referred to as participation banking, which involves participating in businesses. Regular banks guarantee returns to their depositors and use their capital to cover losses. Participating banks have shareholders who share in the profits and the losses. These two bank types should remain separated, even though one bank might offer both in distinct accounts. A commercial bank’s funds should be used only for lending. The maximum interest rate limits lending, allowing equity to replace debt in the financial system.

Evidence from history

There is little historical data on the subject of interest-free demurrage currency. Financial systems founded on interest-free money with a holding fee have never existed. There were holding fees and interest bans, but the combination of both has never existed. More importantly, a usury-free financial system requires a high-trust society founded on moral values where investments are safe, and is only feasible with the help of several relatively modern financial innovations. That all seems too good to be true, but we can have dreams. And so, the evidence from history is of limited value.

Several ancient societies have seen usury-induced economic crises. Extreme wealth inequality, often accelerated by usurious lending, regularly coincided with societal collapses. It is a recurring pattern that has existed since time immemorial. The Sumerians were already familiar with charging interest and its disastrous social consequences. Sumerian rulers began implementing debt jubilees as early as 2,400 BC, cancelling debts and freeing debt slaves. Other cultures, such as those in Israel, have banned charging interest. Israel also had debt jubilees every fifty years.

The Egyptian grain-backed currency existed for over 1,000 years, suggesting it provided monetary stability. Nevertheless, ancient Egypt has seen economic crises, often due to droughts causing crop failures, high taxation during warfare, or a weakening central government. The government mitigated famines with its grain reserves, but prolonged famines depleted these facilities, leading to civil unrest and, sometimes, a collapse of order. There is no evidence of social benefits of this money for Egyptian society. Charging interest was common, and Egypt had debt cancellations.

In the Middle Ages, the Church forbade charging interest. Christians, like Jews, were each other’s brothers and couldn’t charge each other interest. When economic life became more developed, the ban on interest became difficult to enforce. In the 14th century, partnerships emerged where creditors received a share of the profits from a business venture. As long as the share remained profit-dependent, it was not illegal, as it was a participation in a business rather than lending at interest.1 Islamic finance works with similar principles.2

In the 17th and 18th centuries, interest ceilings replaced bans. To circumvent the interest ceilings, a creditor and debtor could secretly agree on a fraud, whereby the creditor handed over less money than stated in the loan contract, so that the borrower actually paid more interest.3 More recent experiences with Regulation Q in the United States, which imposed maximum interest rates on bank accounts, suggest that a maximum interest rate is enforceable only if it does not significantly impact the bulk of borrowing and lending.4

An effective ban on usury requires a society grounded in moral values rather than profit. It requires us to live modestly and within the planet’s limits. It also requires societies to care for vulnerable individuals, so that they don’t fall prey to usurers. You shouldn’t charge interest, not merely because it is illegal, but because it contributes to something profoundly evil. That points to a broader problem. We should care about the world and consider the consequences of our actions. Even when what we do is legal, it doesn’t mean that it is good.

Implementation

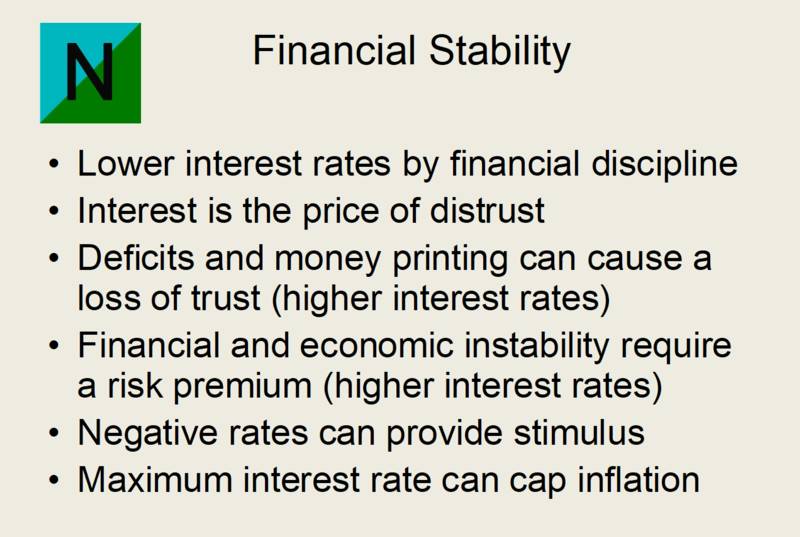

To implement Natural Money, interest rates must already be low or negative. Attempting to lower interest rates when market conditions don’t justify that move would likely scare investors. Low interest rates require trust, which requires financial discipline, including fiscal discipline from governments. That doesn’t equal austerity, since governments earn interest on their debts when interest rates are negative. The transition preferably is a gradual process that the authorities communicate in advance. Whether that is possible at all remains to be seen, as the implementation may occur in exceptional times.

If there is still a functional currency, the first step is for the government to balance the budget. The second step is to decouple cash currency from the administrative or central bank currency. The move encompasses retiring central bank-issued banknotes and replacing them with treasury-issued banknotes. Not everyone will hurry to a local bank office to exchange banknotes, so the central bank-issued banknotes must be exchangeable at par for the new banknotes for a considerable period.

As long as interest rates are significantly above zero, a holding fee won’t bring them down. Setting a maximum interest rate can lower interest rates by curtailing credit, thereby cooling the economy. To avoid disrupting financial markets, the implementation must be gradual. The maximum interest rate should be high enough to avoid disrupting the economy. Initially, authorities could set the holding fee at a low percentage, or not at all. As interest rates fall, authorities can lower them.

The zero lower bound is a minimum interest rate. It operates like a price control by preventing interest rates from moving freely to the rate where supply and demand for money and capital balance. That is to the advantage of the wealthy, as they can take the economy hostage by demanding a minimum return on their investments. When returns are low, investors may prefer cash over investments, which can hinder an economic recovery. Economists call it liquidity preference.

Low interest rates can prompt lenders to seek higher yields and take on more risk. Low interest rates allow borrowers to take on more debt. Low interest rates can promote investments that become unprofitable when the economy slows down. A maximum interest rate can prevent these situations from happening. A maximum interest rate caps the risk lenders are willing to take and promotes a deleveraging of balance sheets, so that even low-yielding ventures don’t go bankrupt because of interest-bearing debts.

Issues with the maximum interest rate

A holding fee will cause few difficulties, but a maximum interest rate is more problematic. Insofar as the maximum interest rate affects questionable segments of credit, such as credit card debt and subprime lending, this is beneficial overall. More serious issues can emerge with financing small and medium-sized businesses. Partnership schemes can fill in the gap, but it is hard to predict how that will play out. The maximum yield on loans is zero, making partnerships more attractive, as they can offer higher returns.

There may be objections to the limits Natural Money imposes on consumer credit. Still, there is little doubt that a maximum interest rate can improve consumers’ purchasing power, as borrowers won’t have to pay interest. As a result, there are fewer borrowing options, which may lead to the emergence of black markets. To make illegal schemes unattractive for lenders, lenders who charge interest could lose the money they have lent.

Zero is the only non-arbitrary number, making it more difficult to change the maximum interest rate. That may happen for political or other reasons. The salespeople of usury can find plenty. If it is one, why not two? Zero is a clear line. A positive interest rate, no matter how small, contributes to financial instability. All positive growth rates compound to infinity, so once we start the fire of usury, it will eventually consume us.

A maximum interest rate seems feasible if it is above the rate at which most borrowing and lending occur, thereby limiting the effects on liquidity in the fixed-income market. A maximum interest rate creates room for alternatives, such as private equity and partnership schemes. These alternatives can supplement the fixed-income market and mitigate the effects of the maximum interest rate. A maximum interest rate is beneficial overall if it mainly affects questionable segments of credit, such as subprime lending.

In the case of bonds, the maximum interest rate of zero applies at the time of issuance. Due to economic circumstances or issues with the debtor, the interest rate may rise and enter positive territory. Likewise, governments may issue long-term bonds that may have positive yields if interest rates rise later on. That is not a serious issue, as long as the interest rate was zero or lower at the time of issuance.

A more serious issue is the risk of liquidity problems. When interest rates rise, less credit becomes available at interest rates of zero or lower. Interest rates might increase due to a strong economy with inflationary pressures. There are always economic agents that must borrow at all costs to meet their present obligations, so if they can’t borrow, they might go bankrupt. Businesses and individuals need to deleverage and arrange credit in advance, such as an overdraft facility, with their banks.

Another equally serious question is the profitability of banks with Natural Money. The lending business of banks will likely shrink significantly. The assumption is that risk-free lending will be profitable. But what if it isn’t? In that case, banks may need to lower the interest rates on deposit accounts to a level below the interest rate on short-term government debt. In that case, the cash interest rate may need to be lower than the interest rate on short-term government debt to make it work.

Inherent stability

Ending usury is impossible without investors having trust in the political economy or the political and economic institutions of the polity issuing the currency. The most trusted political economies have the lowest interest rates because their governments are fiscally responsible. Natural Money requires taking it to the next level. With Natural Money, to borrow, the government must find lenders willing to lend in the currency at negative interest rates. The government will be better off borrowing at negative interest rates, which provides an incentive for budgetary discipline. That is the foundation of stability.

Extracting a fixed income from a variable income stream contributes to financial instability. Fixed interest payments can bankrupt a corporation even when it is profitable overall. Interest contributes to moral hazard, as it serves as a reward for taking risks. Investors expect to earn higher yields on riskier debt, so lenders take on these risks. The more uncertain an income source, the higher the interest rate needs to be to compensate for the risk of lending, but the higher the fixed interest rate, the more likely failure becomes, which reveals the destructive consequence of interest being a reward for taking risks.

All parts of the financial system are intertwined. Individual banks can transfer these risks to the system. And so, the risk management of individual agents can increase the overall level of risk in the system. The payment and lending system is a key public interest, so governments and central banks back it. Banks take risks and reap rewards in the form of interest, while public guarantees back up the financial system. The arrangement leads to moral hazard, a mispricing of risk and private profits at the expense of the public. A maximum interest rate can end these problems.

A maximum interest rate causes a deleveraging and a reduction in problematic debts, which has a stabilising effect on the financial system and the economy. Individuals and businesses must already take action before their debts become problematic. Maximum interest rates can distort financial markets. Most notably, there will be fewer options for smaller firms to borrow. Partnership schemes should fill that void.

Interest payments also affect business cycles. The mainstream view is that central banks should raise interest rates during economic booms to curb investment and spending, thereby preventing the economy from overheating. A rosy view of the future prevails during a boom, so higher interest rates seem justified and borrowing continues for some time. When the bust sets in, the picture alters, and an overhang of debt at high interest rates worsens the woes. It would have been better if these debts hadn’t existed in the first place.

That makes a usury-based financial system inherently unstable. Natural Money changes this dynamic. When the economy improves, higher interest rates increase the attractiveness of equity investments relative to debt. That reduces the funds available for lending. The curtailment of credit will prevent the economy from overheating and avoid a debt overhang. When the economy slows, negative interest rates provide stimulus. In the absence of a debt overhang, the economy is likely to recover soon. A Natural Money financial system is inherently stable.

Featured image: 1919 Cover of The Natural Economic Order. Wikimedia Commons.

1. Simon Smith Kuznets, Stephanie Lo, Eric Glen Weyl (2009). The Doctrine of Usury in the Middle Ages. Simon Smith Kuznets, transcribed by Stephanie Lo. An appendix to Simon Kuznets: Cautious Empiricist of the Eastern European Jewish Diaspora. 2. Sekreter, Ahmet (2011). Sharing of Risks in Islamic Finance. IBSU Scientific Journal, 5(2): 13-20. 3. K. Samuelsson (1955). International Payments and Credit Movements by the Swedish Merchant Houses, 1730-1815. Scandinavian Economic History Review. 4. R. Alton Gilbert (1986). Requiem for Regulation Q: What It Did and Why It Passed Away. Federal Reserve Bank of St. Louis.

Before the Industrial Revolution began in England, European crafts and sciences had already advanced. During the Middle Ages, inventions such as gunpowder, eyeglasses, the compass, the printing press, the mechanical clock, the windmill, and the spinning wheel had reached Europe from China or the Middle East. What made Europe culturally different was its individualism. In the 14th and 15th centuries, a new spirit emerged in Italian merchant towns like Venice, Florence, and Genoa. It was the spirit of the merchant which subsequently spread throughout Europe.

And so, Europeans gradually abandoned their traditional Christian values and developed a capitalist spirit by pursuing worldly wealth and pleasure rather than modesty and bliss in the afterlife. There were merchants elsewhere, but the populace held them in low regard because of their depraved ethics, as greed was their core value. It was the pursuit of profit that drove European explorations and colonialism. Making money became the new moral virtue, alongside inquisitiveness, creating a dynamic that would change the world.

During the 16th and 17th centuries, Europeans explored the world and invented the microscope, the steam turbine, the telescope, and the steam pump. Modern science began when Nicolaus Copernicus calculated the trajectories of the planets by assuming that they revolved around the Sun. Isaac Newton later formulated the laws of motion. Europeans expanded their colonial empires, thereby increasing the size of their markets, a prerequisite for the mass production that industrialisation was to bring.

The British were the most successful. Supported by a strong navy, they built the largest colonial empire. They also invented modern banking, creating money out of thin air or financing capital by imagining future revenues. In 1689, the British had the Glorious Revolution, which, like many revolutions, was about taxation. Businesspeople then took over the government. Taxation henceforth required the consent of the taxed, thus, property owners. And the state became a venture of the propertied classes, like the Dutch Republic, the wealthiest nation at the time, already was.

The taxpayers didn’t like to pay for ineptitude and corruption, so the quality of the British state improved, and the state used its military to support the colonial business ventures of the propertied classes. Great Britain had easily accessible coal deposits and developed a large coal mining industry. Due to a lack of firewood, coal had become England’s primary heating source. As mine pits grew deeper, they became prone to flooding. With no transport costs, a coal-fired steam engine to pump water out of the mine became cheaper than manually pumping with buckets.

Ignition

Trade with the colonies promoted British industries, resulting in high living standards and wages in England. In England, coal was easily accessible, so energy was cheap. In Great Britain, the aristocracy had an entrepreneurial spirit and paid taxes, making the British government a reliable borrower. Banking innovations, most notably the creation of money, made British capital markets more efficient. And so, Great Britain had low interest rates, so a low price for capital. The first machines were clumsy and inefficient, but high wages, cheap capital and affordable energy made them profitable.

This combination of factors is why the Industrial Revolution started in England rather than elsewhere. Wages in France were lower, while the banking system was less developed. The rent-seeking French aristocracy didn’t pay taxes, making the French government an unreliable borrower. Thus, interest rates in France were higher. Once the first machines were in operation, inventing new ones or improving existing ones became profitable, so British engineers got busy enhancing the steam engine’s efficiency and inventing contraptions like the spinning jenny and the cotton gin.

The fuel consumption of steam engines dropped from 44 pounds of coal per horsepower-hour in 1727 to 3 pounds in 1847, making it economical to use the steam engine for other purposes, such as trains. The dramatically improved fuel efficiency, combined with other improvements, made it economical to mechanise production elsewhere where wages were lower, interest rates were higher, or energy was more expensive. That allowed the Industrial Revolution to spread to other countries.1

It was a watershed moment. Until then, inventions were rare. Scientists made them out of curiosity. However, from then on, the profit motive generated a permanent drive to pursue knowledge and new technologies and to invent new products. In this way, economising through innovation and scale became a constant, unstoppable process that economists call creative destruction. Factories needed scale to operate profitably, while inventions birthed new industries and made others obsolete.

Humans have started a fire in their midst that continues to grow. We can’t stop it. A classic book on the Industrial Revolution used at universities is David Landes’ The Unbound Prometheus. According to Greek mythology, Prometheus stole fire from the gods and gave it to humans. The Greek supreme deity, Zeus, punished him for his act. The story parallels the biblical story of the Fall. The Industrial Revolution unleashed the unlimited fire of the gods that will devour us.

Since the Industrial Revolution, the general level of opulence has risen dramatically, though it was hardly noticeable at first. Industrialisation made craftspeople in the clothing industry destitute as they couldn’t compete with factories. Everyone else profited from cheaper cloth. Mechanisation made existing products like cloth more affordable, so people had money to spend on new products like light bulbs, making investing in new inventions profitable. Economists call it Say’s Law. More supply generates new demand.

Due to these innovations, production costs decreased, and industrialisation became profitable where wages were lower, energy was more expensive or interest rates were higher. Industrialisation first took off in Europe and North America, but not elsewhere. One reason is that Europeans had become innovation-minded and eagerly adopted new technologies like railroads and telegraphs. These first technologies were simple, thus easy to apply, but the Chinese and others remained reluctant to use them.2

Standard development recipe

Western Europe followed quickly, helped by the French Revolution and Napoleon Bonaparte’s reforms. The French Revolution wiped out the corrupt old French regime and replaced it with a modernised, efficient bureaucracy. The aristocrats lost their power. The French introduced civil registries, rationalised the law code, standardised weights and measures by introducing the metric system with kilograms and metres, and made everyone drive on the right side of the road. Napoleon’s armies then spread these reforms over Europe. Napoleon did to Europe what the first Chinese emperor did to China 2,000 years earlier. Both reigned shortly but left a lasting legacy.

Countries Napoleon didn’t conquer, such as Great Britain, continued to drive on the wrong side of the road and use arcane measures like miles and ounces. And only in Great Britain do aristocrats still influence politics through the House of Lords. To catch up, Western Europe and the United States followed a standard recipe consisting of the following elements:

Creating a national market by eliminating internal tariffs and building railroads.

Developing domestic industries by using external tariffs.

Instituting banks to finance investments and stabilise the national currency.

Establishing a mass education system to upgrade the labour force.

These measures had enormous social consequences, which we now refer to as modernisation. Societies came to replace communities. It was the age of nationalism. With the help of mass education, everyone learned the national language, and local dialects disappeared. People learned to identify with their nation rather than their kin and village. The outcome was that modern humans rely on markets and the state more than on their family and community.

Other countries implemented the same recipe but with modifications due to local economic factors. Factory layouts that operated at a profit in Europe were loss-making elsewhere. If energy were expensive, the operation would become more cost-effective using fewer machines and more labour. Japan was the first non-Western country to follow. The Japanese had to deal with local circumstances. High interest rates made investment capital expensive, so Japanese factories held no stockpiles of raw materials and semi-finished products but let their suppliers make them when needed. So, when interest rates rose in the late 1970s and early 1980s, Western industries couldn’t compete with Japan.

There are varying views on why industrialisation succeeded in some countries but not in others. If you dare to generalise, you can make the following observations:

East Asian countries like Japan, South Korea, Taiwan, and later China modernised successfully. They had a sense of nation and experience with rational government administration. Their bureaucrats and businesspeople successfully implemented modernisation projects.

Latin American countries were less successful. They were former colonies lacking national identities. Their white elites neglected the education of indigenous people. There were a few large estates and hardly any small-scale farmers. Wealth inequality prevented the development of a middle class.

The Soviet Union modernised with the help of state planning. Industrialisation of heavy industries succeeded, allowing the Soviet Union to defeat Nazi Germany. Agricultural reforms were a disaster, and consumer products were of poor quality. By the 1970s, it became clear the Soviet Union couldn’t keep up with the West.

Several countries in the Middle East modernised with dictators implementing socialist development models based on the experiences in the Soviet Union. Some Arab countries became wealthy from oil revenues. Few countries in the Middle East have developed industries that compete in international markets.

Africa lagged. African borders didn’t match the tribes living there, so there was no sense of nationhood. There have never been states in most of Africa. European colonisers ended traditional forms of government and property rights, contributing to poor governance and corruption. Africans started with a disadvantage.

Industrial politics

There are requirements for a modern economy, though a country doesn’t need to meet all of them. A capable government and an educated workforce can turn a situation around. Japan has few natural resources, but has become one of the most advanced countries in the world. It was the first non-Western country to industrialise. Japan was also lucky. After World War II, it had access to US markets because it was a close ally of the United States, which needed it to help it export its way into prosperity. Argentina had fertile land and was one of the wealthiest countries by 1900, but it has since then gone downhill. To successfully modernise, a country probably needs:

a capable government that understands economics and is business-friendly

an educated workforce as workers must read, write and use technology

businesspeople, investment capital, and sufficiently ensured property rights

a large enough market, thus a sizeable middle class

an industrial policy, thus picking industries to compete in international markets, helping to develop them, and supporting them with tariffs or subsidies

There are several kinds of industrial politics. Neo-liberal politics aim to pursue economic growth by promoting trade, lowering taxes, and reducing regulations. Unrestricted trade allows areas and people to specialise and compete to produce more and better products, enhancing overall opulence. It also promotes a race to the bottom at the expense of our future. Industries go where wages are lowest or where they can dump their waste and avoid paying for government services.

Making the economy sustainable and people-friendly also requires industrial policies, such as reducing competition and introducing regulations and controls. And it requires ending imports from countries that don’t adhere to the same ethical standards. A sustainable, people-friendly economy can only exist on a level playing field with other economies that adhere to the same standards. These measures increase costs and reduce living standards. An extreme case is the Old Order Amish. They choose to be self-sufficient and live simple lives. Their economic model resembles community economics.

Community economics aims to enable people in a community to help each other by buying and selling goods and services using local currencies. It never became a worldwide success because communities lack the scale for self-sufficiency. There is also a lack of commitment, which is something the Amish do have. Few people barter their labour or goods in their community if they can get better deals elsewhere. Commitment is vital. Without it, there will be black markets with merchants smuggling in illicit goods.

Featured image: Amish family, Lyndenville, New York. Public domain.

1. The British Industrial Revolution in Global Perspective. Robert C. Allen (2014). Cambridge University Press. 2. Sapiens: A Brief History of Humankind. Yuval Noah Harari (2014). Harvil Secker.

Mainland Europe and the Anglo-Saxon world, and most notably, the United States, are culturally related but have significant differences in views on law and morality that underpin their societies. These differences greatly influenced history, but their causes also lie in history. In the Middle Ages, individualism was already strong in Western Europe. While England developed its law system, the bureaucracy of the Catholic Church introduced Roman civil law on the continent. It had the following outcome:

Common law has become the basis of law in Great Britain and many of its former colonies, including the United States. Individuals are sovereign. Common law works bottom-up by generalising rules from judges’ verdicts in individual cases.

Civil law has become the basis of law in mainland Europe and most other countries. The lawmaker is sovereign, thus the king or the people as a collective via parliament. It works top-down by applying general rules to individual cases.

Common law resulted from the efforts of English kings to build a coherent law system based on local practices. In 1215, the Magna Carta limited the power of the English kings. England then had a strong state where the rule of law limited the king’s power. There also was individual liberty in Western Europe. There were few strong states while merchants ran independent cities. Still, the rule of law later came from the state’s power because of the differences in law foundations. These differences relate to views on ethics:

In Great Britain, philosophy, including ethical philosophy such as David Hume’s, is pragmatic. It says moral rules are an agreement in society, so good and evil depend on popular sentiments, freedom is being able to do as you please, and outcomes matter more than intent.

In continental Europe, idealism dominates philosophy, including ethical philosophy, such as that of Immanuel Kant. It says good and evil are absolute, freedom means liberating yourself from your lower urges, thus becoming rational and morally upright, and intent matters more than outcomes.

If ethical rules are relative, they emerge from popular sentiments, thus bottom-up, and if they are absolute, they come from principles and work top-down. The English philosopher John Locke imagined the state as a voluntary agreement of individuals to cooperate for mutual benefit. If you believe in individual sovereignty and moral relativism, that must be why there is a state. But it is incorrect. We will not voluntarily agree to a state if there is none but fight each other until there is one.

These differences later shaped the debate on the economic system, hence the intellectual battle between capitalism and socialism. Adam Smith wrote a practical recipe for running an economy in the British tradition. In continental Europe, the debate became fundamentalist and infused with moral sentiments. Frédéric Bastiat claimed socialism is an organised plunder of private property, while Karl Marx argued that capitalists steal the value workers create.

In the United States, with its moral pragmatism founded on individual freedom, the collectivist ideology of socialism never caught on. Still, progressives in the United States pursued reforms to rationalise the government according to modern bureaucratic principles, and there were unions. Great Britain became caught in the middle as Brits had a more favourable view of government than Americans and a strong socialist movement.

When, after World War II, the Soviet Union became an existential threat to the United States because the communists planned to overturn the capitalist order with violent revolutions and were building a large army, the defence of individual autonomy and moral pragmatism itself turned into an idealist moral crusade, also because the Soviets aimed to end religion and persecuted religious people. Most US citizens identified as Christians, so they came to see the Soviet Union as an evil, godless empire.

Hegelian Dialectic and Marxism

Around 1807, the German idealist philosopher Georg Wilhelm Friedrich Hegel devised a theory of how history would unfold according to God’s plan. It would occur by challenging the prevailing ideas and social order. The French Revolution had just swept away the old aristocratic French regime. The French adopted revolutionary new ideas from the European Enlightenment, modernised their government and introduced an army of conscripts, allowing Napoleon to conquer Europe and spread these ideas and reforms. Hegel was the proverbial fly on the wall, taking it all in. He was impressed. That was progress! Modern ideas wipe out old ones. A bureaucratic government with conscripts eliminated an aristocracy with mercenaries. The German Christian idealist philosophers like Kant and Hegel, and later, atheists like Marx, Nietzsche, and Heidegger, dedicated themselves to hard questions pragmatic people would never bother to spend a lifetime on.

As a profoundly religious man, Hegel thought that our knowledge and ideas progressed and that God’s plan worked like so. He believed humanity had a collective consciousness in which these ideas reside. He surmised we are progressing towards our final destination, God’s Paradise, by replacing our prevailing ideas with better ones. An example is our views on slavery. Slavery existed since time immemorial and was generally accepted, but most of us now see it as evil. These views we all share are what Hegel meant by collective consciousness. It evolves over time and thus progresses according to a stylised scheme called Hegelian dialectic. It works like this:

(1) there is a status quo (the thesis) (2) new ideas or conditions challenge the status quo (the antithesis) (3) from the challenge emerges a new status quo (the synthesis)

A synthesis is a more profound truth rather than a compromise. You can’t bargain on the truth. Hegelian dialectic is a ruthless pursuit of truth and accepting its consequences. Hegel is the philosopher of progress, not economic or scientific, but progress in society and its institutions. It is nearly impossible to overestimate his influence on politics in the centuries that followed as it often was about progressives versus conservatives, thus applying new ideas from philosophy and the sciences versus keeping things as they are. Not all new ideas are better, so the outcome can be that nothing changes. Ideally, the synthesis is the best solution that emerges from the challenge of the status quo. If the new ideas are superior, they wipe out the old ones. That requires revolution and violence, such as the French Revolution and the Napoleonic wars.

Being more pragmatic, the British reformed in smaller steps. The principal problem with Hegelian dialectic is that the scheme can have disastrous consequences if you don’t know everything. Your logic can be perfect, but if your assumptions are not, a small oversight can cause ruin, as in Barataria. Chaos theory says why. The leading conservative British thinker, Edmund Burke, aimed to improve the government, but only if necessary, because changes have unpredictable consequences. The British could do that because they already had a government open to reforms, while the French did not. A revolution was their only option to rid themselves of the corrupt old regime and clean the slate.

Karl Marx took the bait. We could achieve paradise ourselves here on Earth, he claimed. Scholars had already found out that much of the Bible was fiction, and Charles Darwin had just published On The Origin of Species with evidence indicating plants and animals emerged in a competition between species that has lasted millions of years rather than being created in six days 6,000 years ago. The sciences had proven religion wrong, so Marx thought religion keeps people dumb. Christians would wait for Jesus, who hadn’t shown up for over 1,800 years, and not take matters into their own hands. Marx also noted that Christians had betrayed their religion by adopting the ethics of the merchant. According to Acts, early Christians lived like communists.

Marx claimed capitalists profit by stealing some of the value workers create. He based his allegation on the labour theory of value, which economists of his time considered valid. The theory says that the price of an item equals the cost of labour required to make it, thus including the labour to produce the raw materials. If making a pair of shoes takes twice as much labour as making a pair of trousers, shoes cost twice as much as trousers. Marx then asked, ‘If that is correct, how can there be profits?’ It is because the theory is wrong. There is no objective measure of value. In a market economy, the price of an item depends on what people are willing to pay for it, not what it costs to make it. Otherwise, you could work a year on building a better mousetrap and sell it for € 50,000. Perhaps, after spending another € 50,000 on building a brand in a marketing campaign, you can sell it for € 200,000. That is how markets work.

Value is what we believe it is. Nothing is sacred. Everything is for sale, including the rainforests and even the Earth. The so-called owners think it is all theirs and can do with it as they please. In the market, a message becomes true if you can sell it. It works with advertisements or denying climate change. It is the evil in the ethics of the merchant, and because money represents power, we stare into the moral abyss. If you ever wonder why communists called their newspapers The Truth, that is why. But in a world without God, there is no truth, and communism is just another message on the marketplace. The communists appealed to the workers’ self-interest. And that was a poor sell because workers were worse off under communism. It is why communism was doomed to fail, not because it is impossible to live like communists. Early Christians did. Rather than concluding he had just proven the labour value theory wrong, Marx claimed capitalists stole from their employees.

Marx further said that producing for markets alienates us from what we make. Many workers experience this. It is why Dilbert comics are so successful. Marx claimed we could be free, creative beings, but the modern, technologically developed world dictates our lives. Marx believed ending the market mechanism and replacing it with democratic planning would liberate us. So if workers received what they owed and we replaced capitalism with democratic planning, we would live in a paradise where we can do the jobs we like and have everything we need. That is a silly idea. Many want to be a Hollywood star, but few want to be a cleaner. Immigrants do those jobs. Communes don’t attract farmers and construction workers but artists and reiki healers. We need food and homes, not art and quacks. Work is doing something useful, and if it isn’t useful, it isn’t work. And even if everyone contributes, planning will never do as well as markets. You could live with that if you have enough. You might want a pear, but you could settle for an apple. And you have heard of oranges but never tasted one.

Marx also claimed that capitalism causes misery as adding capital means doing more with fewer workers, which reduces the need for labour, pushing wages below the subsistence level and leaving workers to starve. At the time, most economists believed wages would remain close to the subsistence level. If wages increased, more people survived, expanding the labour supply. And so, wages would decrease, and more people would starve. The market would keep population levels in check. Marx argued that making more stuff with fewer people was impossible because the unemployed couldn’t buy it, and capitalism would bankrupt itself. It didn’t happen because of Say’s Law, as things became cheaper. And we can create money from thin air. When capitalists produce more, they must sell their merchandise, and you can make people borrow money, so the general level of opulence rises. Marx vastly underestimated human ingenuity in finance, marketing and job creation in the services sector and government, the so-called bullshit jobs in the bullshit economy. These jobs make sense because they solve problems in our complex society, but we could do without many of them when we live simpler lives.

Marx believed he was scientific and rational. He devised a theory of history using Hegel’s dialectic, arguing that power structures in society reflect economic conditions. To Marx, it was not new ideas challenging the status quo but economic conditions driving change in history. He would say that the status quo of serfdom in Europe ended because towns challenged it by providing alternative jobs for serfs. Lords had to compete with them for their labour. And so, employer-employee relationships replaced serfdom, which became the new status quo. Marx also believed nationalism was a temporary phase, as economic conditions imposed it on us. Industrialisation required larger markets, thus societies rather than communities. Nationalism allowed the elites to divide and rule the working class. And because capitalism would eventually bankrupt itself, Marx predicted, as if it was a logical certainty, communism would replace employer-employee relationships, and everyone would become free and equal. In reality, people aren’t free or equal under communism, and a new elite of party bureaucrats replaced the capitalists.

Marx’s plan for the future included violently overturning the existing capitalist order in revolutions like the French Revolution and Napoleonic wars. Karl Marx became the prophet of the most successful cult in recent history. Despite the failure of communism, the capitalism-socialism debate continues because Marx raised pressing concerns that are still valid today:

Instead of saying capitalists steal value from workers, you can argue we work to make the rich richer. Despite stellar economic growth in the United States, many workers still can hardly get by. And that is not because they are all lazy or stupid.

Instead of saying the system alienates us from what we produce, you can argue we are part of a system over which we have no control. We can’t democratically decide on issues like implementing artificial intelligence.

Instead of saying capitalism causes misery, we can argue it improved billions of lives, but it probably ends in a total disaster. We may know for sure once the ecological or technological apocalypse materialises.

Instead of saying we will enter the communist paradise as a historical necessity, we may argue the script is that we are about to enter God’s Paradise, which could be a Hegelian synthesis of Marx’s challenge of the existing capitalist order.

The moral void

European moral idealism and American moral relativism have consequences you might not think of. German philosophers from the Frankfurt School, knowing our religion, if we have one, depends on our birthplace, that Jews invented the Abrahamic God and that much of the Bible is fiction, sought more absolute foundations of morality, such as equality or preventing harm to other people. They embrace LGBT rights like marriage, as there is no objective moral reason to deny them. Even if you think gay marriage is unnatural because a gay couple can’t produce offspring, there still is no objective moral reason to deny them these rights, no matter what the Bible says. Idealism also drove Germans to endanger their energy security by closing nuclear plants and betting on solar and wind.

American moral relativism drives conservative Christians to impose their views on others, as they don’t ask hard questions, ignore evidence contradicting the Bible, and think they can do as they please rather than act as a rational, morally upright person. Critical theory, thus cultural Marxism or Woke, comes from German philosophers daring to ask hard questions to seek the absolute foundation of morality. Critical theorists also indulge in speculation. Many of their theories lack solid evidence. Believing, like Marx, that their ideas are superior, the Woke use Hegelian dialectic to attack conservative Christianity and impose their views on society. That is why Woke people are so annoying. In recent years, that debate has escalated rather than synthesised. It has turned into a culture war.

Conservative Christians, most notably those in the United States, are a peculiar bunch. Humans are the most destructive species that ever roamed the Earth, and there are far too many of them, so it is evil to ban abortions. If there is a moral objective measure for preserving a life, it is its degree of sentience. A human newborn can only suck milk, and no one remembers being born, while cows, horses and pigs stand upright and walk after birth. A cow or a pig is more conscious than a ten-week-old fetus, yet we slaughter them by the millions after treating them horribly in conditions as miserable as concentration camps. It is a Holocaust. You can better be dead long before you are born. Christians corrupted Jesus’ teachings to take away women’s rights and claim trans people are evil after giving God a sex change. They harp about an alleged conspiracy of Satanic child molesters in government while electing a sex offender who regularly attended Epsteins parties.

Liberals might think many Christian conservatives are crazy to believe raving nutcases like Qanon, but we cooperate using shared imaginations, so it is perfectly normal human behaviour. How do you think religions survive despite the facts disproving them? And the only measure of success is success. Truth hardly ever is the reason why beliefs prevail. Even scientists have invisible imaginary friends like gravity. Believing that gravity exists makes you succeed in engineering. The foundations of liberalism and socialism are also incorrect, like human nature being inherently good. We like to think we are good, so these ideologies have been successful. And success breeds stupidity. If you fail, you might ask the correct questions, but when you are successful, you have no reason to. And so, rational government is an uphill battle against our inner nature, and real change is only possible after complete failure. Christianity is much closer to the truth. We are morally depraved, incapable of fixing ourselves, unworthy of God’s grace, and in need of a saviour.

Liberals are wrong and foolish because the evolution theory they believe in says the struggle for existence is brutal. They should have reasoned, like Friedrich Nietzsche, that God is dead and that the strong should rule the weak. Somehow, they couldn’t rid themselves of their Christian slave morality. The former right-wing Dutch politician Pim Fortuyn called them the Leftist Church. Without God, we get lost in the moral void, and it is pointless to try to achieve Paradise on Earth. After several wars to impose liberal Western values on countries like Vietnam, Iraq and Afghanistan, we can say good intentions usually make things worse rather than better. Why send money and weapons to a corrupt country like Ukraine to let it fight against an even more corrupt country like Russia? And why do liberals support the corrupt establishment of big banks, big pharma, the mainstream media and the military-industrial complex they objected against in the past? But many Christian conservatives don’t even make a small effort to become slightly less evil, like skipping meat one day per week. Appeals to moral reason infuriate them. And now the crazies organise a witch hunt against science and the rule of law. The road to hell may be paved with good intentions, but being intentionally evil is a shortcut.

Suppose Jesus was human like us with the knowledge of his time, which non-religious biblical scholars would agree on, and someone else finds himself in his position today. What could he do? He could wait for God to tell him, but if God doesn’t, he might think, like Marx, that he has to figure it out himself. As far as we can infer from the scriptures, Jesus acted independently but according to God’s will. He was like an actor following a script. His successor has the benefit of today’s knowledge, including the simulation hypothesis and the sobering outcome of the communist experiment. He might grasp the greater picture. The Marxist challenge of the existing order could have been God’s way of showing us the choices we face, our alternatives, their consequences, and what the synthesis might look like. That makes Hegel one of the greatest prophets of modern history.

Most people in the West now believe there is no alternative to capitalism, even though we may need some socialism or government to contain its ills. That could make our economy less competitive, which could cause us to lose the competition. So, in the end, there is no alternative, not because we can’t live happily in another economic system but because other systems can’t compete. Other ethical systems can’t compete with the ethics of the merchant either, which says you can do as you please and take what you can. It is much easier to break a collective effort like combating climate change than to build it. Only one major country needs to step out. In competition, those with the most depraved ethics win. The Dutch would say the merchant always wins from the vicar.

Only there needs to be an alternative. The profit motive is the severest threat humanity has ever faced. It pushes for permanent innovation, a process of creative destruction over which we have no control. We have started a fire in our midst that grows until it consumes us. Our greed is its fuel, and we can’t stop it. We may soon destroy ourselves creatively. We can’t kill the beast, the system, and the beast within ourselves, our greed. Communism is oppressive, kills creativity, and promotes stagnation by eliminating the profit motive. That sounds awesome because that is precisely what we need.

It looks like a cure. If your disease is cancer, and the cure is chemotherapy, you take the poison, and you accept becoming sick and losing your hair. Otherwise, you die. You could visit a witch doctor or a quack, and you also die. Many fall for snake oil salespeople because science doesn’t always have the correct answers. But despite their limitations, the sciences and the evidence from history are our best knowledge. If capitalism and communism are the only options, a sensible person chooses communism. Communism has brought a lot of misery, and we haven’t seen the end of civilisation yet, so we can still believe it will work out fine as long as markets remain operational and bring together supply and demand. That is perhaps the biggest lie ever.

If you don’t get by now why the ethic of the merchant is the greatest evil of all times, you are a moron, and there is no point in trying to convince you. By electing Donald Trump, Americans demonstrated their willingness to let Satan run their country. If following Satan seems the lesser evil, then something must be profoundly wrong. The corrupt old order of the military-industrial complex, big pharma, big banks and other interest groups seeking to profit from the state has ended the legitimacy of the US government. The other candidate and the billionaires backing her believed they could buy the presidency by spending billions on her political campaign. And for the record, Donald Trump isn’t Satan, not even the Antichrist, but just a huckster with the most depraved moral values and the ultimate embodiment of the ethics of the merchant, the ultimate evil.

In a world without God, there is no justice. And we can’t halt our descent into the moral abyss. And we have the ultimate proof. Once the technology is there, some of us will become like gods, live for thousands of years, make virtual worlds in which they force everyone to comply with their wishes, and murder people for merely standing in the way or for any other arbitrary reason. It is why we exist. God is an individual from an advanced humanoid civilisation who wants to have some fun. You are nothing, even less than a worm, as a genuine worm decides for itself how to grovel and when. Let that be a warning. And you own nothing. Believing you are entitled to something is thinking you can steal from God. With these words, I conclude my sermon. Now, let us pray.

In a world without God, there is no justice. And we can’t halt our descent into the moral abyss. And we have the ultimate proof. Once the technology is there, some of us will become like gods, live for thousands of years, make virtual worlds in which they force everyone to comply with their wishes, and murder people for merely standing in the way or for any other arbitrary reason. It is why we exist. God is an individual from an advanced humanoid civilisation who wants to have some fun. You are nothing, even less than a worm, as a genuine worm decides for itself how to grovel and when. Let that be a warning. And you own nothing. Believing you are entitled to something is thinking you can steal from God. With these words, I conclude my sermon. Now, let us pray.

Third ways

There have been several attempts to come to a synthesis of capitalism and socialism, which is often called the Third Way. The challenge of Marxism, the antithesis of capitalism, fuelled a lively debate about economic systems in the second half of the 19th and the first half of the 20th century. Silvio Gesell, who wrote Barataria, was one of the central figures in this debate, as was Henry George in the United States. Since the Cold War, the debate has narrowed down into a struggle of communism versus capitalism or individual freedom versus enforced collectivism. With the collapse of the Soviet Union, the discussion in the West ended with the conclusion that Marx may have had valid concerns, but we can’t fix them, and his solutions are counter-productive. The Chinese government, however, kept innovating and remained determined to make socialism work.

You can’t compromise with ultimate evil. That reasoning made the Soviets replace markets with state planning. And it made their repression so ruthless and bloody. Millions died of starvation, and millions more ended up in concentration camps. In the end, it is better to be a slave in Paradise than a free man in hell, except when hell looks like Paradise and Paradise is like hell. But profit and greed corrupt everything. Self-regulation under neoliberalism, thus allowing corporations to set and enforce their rules, demonstrated why corporations need a tight leash and operate for public benefit rather than private profit. So, the question remains whether a third way is possible at all. Or can we only make socialism work better and more agreeable?

Such a change requires the support of a large majority of the people. The Russians lost faith in the Soviet experiment as central planning produced poor outcomes. Still, the Chinese economy has baffled the proponents of capitalism. The Chinese allow the profit motive to exist as long as businesses conform to the Chinese Communist Party’s objectives. State ownership of enterprises further ensures that. Similarly, you can allow profit motive within society’s goals and place large corporations in sovereign wealth funds. To clarify the discussion, as there is confusion in terminology, it may be best to provide you with definitions of economic systems. Their differences centre around ownership of resources, capital, and labour.

resources

capital

labour

communism

state

state

state

socialism

state

public

private

third way / mixed

varies

varies

private

capitalism

varies

private

private

Under communism, the state owns everything, including your labour. You can’t even decide on the job you take. Under socialism, you can choose your occupation, but capital is public, thus owned by workers or the state, and the state owns the natural resources. In mixed economies, ownership of natural resources and capital varies. You may own the ground, but if oil is underneath, it may belong to the state. There may be state-operated corporations like railways alongside private corporations. And you are free to choose your occupation. Under capitalism, everything is private. There may be public services, but there are no public corporations. And few countries give their resources away for free, and governments nearly always want a piece of the action. Not even the United States is fully capitalist. Libertarians think that is the problem, so if we gut the government and make everything private, the invisible hand, thus greed and competition, will fix things as if being foolish doesn’t help, being more foolish might.

The same model still gives different outcomes under different circumstances. A crucial factor is the culture or spirit of the nation. There were substantial differences in living standards in the Soviet Block. Czechoslovakia did relatively well. Yugoslavia suffered from high unemployment, but the Slovenian unemployment rate never exceeded 5%, while Macedonia and Kosovo had rates of over 20%. These were extreme differences within one country and the same system. China has developed its economic model, a state-run socialist market economy, which now outcompetes the West. Its success depends on the Chinese people’s hard work and ingenuity, China’s long-standing tradition of a modern bureaucratic government, and Confucianist ethics, making the government work in the public interest. The Chinese had a modern bureaucratic government on rational principles 2,000 years before Europe. And so, this economy wouldn’t have emerged elsewhere.

Making idealism work still requires pragmatism because good intentions can give horrible outcomes. Americans are pragmatic and gung-ho, thus eager to get things done. So once they realise God’s vision for the future goes against some core principles of American society, like individual liberty and capitalism, they might reverse course and take up the challenge with zeal. Europeans are not like that. They have a wait-and-see attitude at best. The Germans will try to engineer an even better system. The Dutch will deliberate the proper procedure and hire consultants to write reports. The Italians will bumble. And the French will go on strike. Many Americans are also more religious and more willing to embark upon an outlandish plan if they believe it is the way forward.

Free Economy

There are other options than communism or socialism. They can be safe as long as the ethic of the merchant doesn’t reassert itself. As soon as you allow it, the moral depravity spreads like cancer and will destroy society, like in the tale about the imaginary island Barataria. Only communism and brute repression are 100% safe. Religion can inspire us to stay public-spirited and be content with what we have. So if God exists and sends a messiah, we could play it less safely because whatever happens is God’s will.

For a while, Barataria had an economy with free enterprise and private ownership of homes but without capitalists, bankers, and merchants. Barataria had no income taxes, but the lands were public, and farmers rented them, which paid for the small government. Because the Baratarians were public-spirited and helped each other, and most notably, because there were no merchants, they didn’t need much government. That might be as close to Paradise as we can get. But it will only work if we live simple lives.

Silvio Gesell believed in economic self-interest as a natural and healthy motive for satisfying our needs by being productive. He aimed for free and fair competition with equal chances for all. He proposed the end of legal and inherited privileges, so the most talented and productive rather than the most privileged would have the highest incomes without distortion by interest and rent charges.

After experiencing an economic depression in Argentina in the 1890s, Gesell found that economic returns sometimes didn’t meet investors’ minimum requirements. It caused investors to put their cash in a vault like Scrooge McDuck, emptying the money flows and collapsing the economy. A holding fee can keep the currency in circulation, as low returns are more attractive than paying that fee, which amounts to a negative interest rate. Gesell’s economic system was well-known in Germany as the free economy.

European Union

European economies are mixtures of capitalism and socialism. Many Brits found the union too socialist and bureaucratic, so they left. These sentiments relate to the age-old differences in law and morality. The European Union tries to tame the beast of capitalism with regulations, which may fail if the competition continues and intensifies, but many Europeans now live a good life. Well-being is hard to measure, but European societies are among the world’s most agreeable if you believe the rankings. And if every country kills innovation with legislation like the bureaucrats of the European Union, we wouldn’t need to fear artificial intelligence, genetic engineering or any other new technologies.

Europe has a collectivist tradition with Christian and socialist roots with worker and consumer protection laws. Europeans live longer than Americans, partly because the European Union has banned unhealthy foods available in the United States. At the same time, governments run the healthcare systems, so most healthcare is for the public interest rather than private profit. In Europe, it is harder for corporations to pass business-friendly legislation by bribing politicians. That is also because Europeans believe in the common good more than Americans do. Like the invisible hand, our imaginary invisible friend, the common good, has a few magical powers.

As in the United States, immigrants do much of the hard manual labour in Western Europe, often for lower wages, without these protections and crammed in poor housing. There is a profit in dodging regulations for shady merchants. Western Europeans may be lazy because they work 36 hours per week and have five weeks of holidays each year. Still, their lives are the closest to what life should be in Paradise, except that European energy and resource consumption require a drastic 75% cut to make their economies sustainable. But if we dismantle the wasteful bullshit economy and set the right priorities, we could work fewer hours than Europeans do today and still have an agreeable life.

Nazi Germany

The Nazis produced an economic miracle during the Great Depression. The success came from deficit spending for rearmament and limiting trade with the outside world, so the expenditures boosted the German economy while not causing trade deficits. It is similar to Keynesian economics. It worked like the miracle of Wörgl, except that the German government accrued a large debt while the council of Wörgl did not.

Factories were idle, and many people were unemployed, so the scheme didn’t result in high inflation. Price, wage and rent controls also helped keep inflation in check, but it hurt small farmers. The Nazi economy was a mixture of state planning and capitalism. Germany was rearming and preparing for war. It was a war economy. Countries organising for war take similar measures to mobilise their industries for warfare.

Yugoslavia

Yugoslavia was socialist rather than communist. It combined state planning with markets and decentralised decision-making or worker self-management. The Yugoslav economy fared much better than that of fully communist countries. The country was more open, and living standards were higher. However, it began to suffer from mass unemployment, and the economy collapsed in the 1980s as it couldn’t compete with capitalist economies. Generous welfare spending further contributed to Yugoslavia’s economic demise.

The oil crisis of the 1970s magnified the economic problems, and foreign debt soared. The country implemented austerity measures like rationing fuel usage and limiting the imports of foreign-made consumption goods. Unlike the Soviet Union, Yugoslavia had been able to feed its people until then. From the 1970s onwards, the country became a net importer of farm products. Yugoslavs were free to travel to the West. Emigration helped the economy by reducing unemployment and bringing in foreign currencies as emigrants returned money home to support their families.

Its openness to foreign competition contributed to the collapse of the Yugoslav economy. Yugoslav consumer products were often inferior to Western products. To compete, businesses laid off workers to become more efficient. The Yugoslav economic system might have worked if all countries had operated their economies like Yugoslavia. Yugoslav products would have sufficed if there were no better alternatives. Mass unemployment might not have materialised in that case, and Yugoslavia could have managed, perhaps, with less generous welfare. That is a few maybes, but it is plausible.

China

The stories of Airbus and Boeing demonstrate that state ownership of large businesses can work better than private ownership. Boeing was the industry leader but ruined itself by focusing on shareholder profits. Reducing quality brought short-term cost savings, boosted the stock price, and generated management bonuses. That seemed all fine until the Boeing aeroplanes began dropping from the sky. The largest holders of Airbus stock are European states, allowing the corporation to focus on long-term goals. The state-owned aeroplane industry is one of the few areas where Europe is still at the top.

Traditional communism gave subpar results, but the Chinese managed to get it right. The Chinese socialist market economy (SME) has private, public and state-owned enterprises (SOEs). China is not capitalist, as the Chinese Communist Party (CCP) retains control over the country’s direction. It is a command state-market economy like Nazi Germany was. Unlike Nazi Germany, which aimed for maximum self-reliance and ran on military spending, the Chinese economy integrated into the world economy and ran on exports. It resembles other Asian Tigers, such as Japan and South Korea.

The CCP’s vision behind starting market reforms is that China was underdeveloped and that a fully developed socialist planned economy would emerge once the market economy fulfilled its historical role, as Marx prophesied. Thus, the CCP believes it has incorporated a market economy into the Chinese socialist system. Others call it state capitalism, as the SOEs that comprise a large portion of the economy operate like private-sector firms and retain their profits without returning them to the government.

China eliminated extreme poverty, which declined from over 90% in 1980 to less than 1% today. It also became the world’s leading manufacturing economy and the world’s leading producer of unnecessary items that end up in our landfills. Despite its leadership in renewable energy and electric cars, China has also become the world’s leader in pollution and carbon dioxide emissions. However, China’s status as an exporter distorts the picture. By importing from China, other economies appear to be less pollutant.

The Chinese economic model forces corporations to align with society’s goals and make profit secondary. At the same time, it achieves acceptable living standards. It is modern and outcompetes the US and European models. If our society’s goals change from growth to sustainability and happiness, the Chinese economic model can help align corporations with public policies. China is a dictatorship, but its economic model will also work in democracies. Airbus provides the evidence.

State control and ownership of businesses, like China’s, also seem to be the only viable way to pursue political goals such as protecting nature and reducing poverty. Business objectives like profit should be secondary to these political goals. With state ownership, you can ban products or subsidise others without harming or favouring private entrepreneurs, thereby removing the incentive for corruption. China is on the right track as political objectives precede profit. And so we have evidence. China’s economy produced spectacular results, so we can have confidence that it will bring us acceptable living standards while allowing us to live in harmony with nature and end poverty.

In the current financial system, central banks manage the money supply via interest rates. When the central bank lowers interest rates, borrowing money becomes cheaper, making it more attractive to go into debt for consumption or investment. As a result, the money supply increases at a faster pace, which then boosts consumption and investment. When the central bank raises interest rates, the opposite happens, and the money supply increases at a slower pace, or even decreases.

Central banks boost the money supply because usury promotes a money shortage. Most money is a debt, on which debtors pay interest. Debtors must return more than they borrowed. That money may not be available if those with surpluses don’t spend their balances, requiring more borrowing to prevent a disruption in the money flows. Classical economics questions this idea. If the money flows become interrupted, sellers lower their prices, and those with money will spend more to pick up these bargains.

Transmission via the bond markets

Based on estimates of future short-term central bank interest rates, financial institutions such as banks borrow short-term money from the central bank at the interest rate set by the central bank to buy longer-term government bonds. If banks expect the short-term interest rate to remain below 2% in the coming year and 1-year government bonds yield 3%, they may borrow short-term money from the central bank to buy these bonds, repay them when they mature, and pocket the 1% difference.

The trade creates demand for these bonds, causing their price to rise and their yield to drop. Perhaps traders stop buying the bond when the interest rate drops to 2.5% because there is always a risk that the central bank will raise interest rates during that year. If 10-year bonds yield 4%, another trader might sell 1-year bonds and invest the proceeds in 10-year bonds, thereby lowering their yield as well. Usually, this happens in future markets, so traders often don’t own these bonds.

Altering markets

Central bank critics argue that they distort markets by eliminating the market mechanism. Central bank interventions have a profound impact on the operation of financial markets. As a result, there is more lending than would have occurred otherwise. Central banks create liquidity in financial markets by providing short-term funds that banks use to buy bonds with different maturities. It allows banks to buy and sell these government bonds, enabling them to match their lending and borrowing needs at any time.

So, how does that work? Apart from lending to customers, banks invest in government bonds, which they can sell at any time, as they can trade government bonds in financial markets. If a corporation requests a one-million-euro loan that matures in five years, the bank might sell a five-year government bond. In that case, the bank eliminates the interest risk, as it knows the amount of interest it would have received by keeping the bond and the interest it will receive from the loan.

In the past, banks had to be careful because they couldn’t borrow easily from the central bank, nor did they invest in or trade government bonds. So, if you applied for a mortgage, the bank looked for matching term deposits. Perhaps you could obtain a 5-year mortgage if there were sufficient 5-year deposits available. If, after five years, the bank lacked adequate deposits, you would not be able to renew your mortgage and might have to sell your home. And so, you would think twice before getting a mortgage.

Economists call these markets inefficient. You couldn’t get a 30-year mortgage. The operation of central banks has altered financial markets, making them more efficient. That can be beneficial for the economy. The Industrial Revolution started in England. England had the most efficient financial markets. The central bank needs the trust of financial markets. Financial markets can lose confidence, which can lead to a decline in the currency’s value. A central bank can try to restore trust by raising interest rates.

Subsidising the financial sector

Central banks reduce the risk of bank failures. When borrowers repay their debts, banks are solvent. However, they may find themselves short of cash in their vaults when depositors withdraw their deposits. Central banks create this money if needed, so banks need less cash in their vaults. Central banks can also rescue banks in trouble, thereby reducing the risk to the broader economy. After all, a financial crisis can lead to an economic crisis, such as the Great Depression. That nearly happened in 2008.

There are public benefits to stabilising the financial system, but these benefits exist due to interest on money and debts, thus usury. Usury creates a shortage of funds that requires management. Central banks subsidise the financial sector in the following ways:

Central banks mitigate the risk of systemic failure, enabling financial institutions to take on more risk and lend more. Banks may make risky loans to profit from higher interest rates, assuming the central bank will bail them out if things go wrong.

Central banks signal their intentions to financial markets. When the central bank intends to change interest rates, it provides advance notice so financial institutions aren’t caught off guard and can adjust their bond portfolios accordingly.

The supply and demand of funds in the financial markets ultimately determine interest rates. Still, these markets would operate differently without central banks, with significantly less borrowing and lending. Central banks make the financial system function more smoothly and reduce the risk of systemic failure. As a result, interest rates are lower than they would have been otherwise.

Central banks are powerful, undemocratic, technocratic institutions. Since the 1970s, they have become independent from governments. Before that time, governments used their central banks to finance their deficits through money printing, leading to inflation and a loss of trust in currencies. Making the central bank independent from politicians and giving it a mandate to keep inflation low was a move to instil confidence in fiat currencies.

The argument in favour of central bank independence is that a government must be trustworthy to its creditors. Creditors, like most of us, don’t trust politicians because they spend other people’s money. Since then, governments have borrowed in financial markets and paid interest on their debts. Central banks still buy government debt and return the interest to the government, which is the same as printing money outright.

Central banks can impede the functioning of financial markets by mispricing risk. Central banks can save banks in trouble by printing money. Without central banks, financial institutions would have to be more careful. Bank failures would occur more often, and banks would pay more interest to depositors to compensate for that risk. That negatively impacts economic growth and leads to crises. That is why central banks exist.

Signalling intentions

Central banks signal their intentions in advance to prevent traders from being caught off guard, thereby avoiding chaos in financial markets. That issue became at the centre of a drama that played out in the UK bond markets in September 2022. Interest rates spiked after the government announced a massive spending package. It suddenly became clear that the Bank of England might have to raise interest rates much further than previously thought to contain inflation. The spending plan caught financial institutions off guard. The Bank of England had to intervene in the bond market to bring down interest rates.

Financial institutions borrow short-term money from the central bank and invest it in the bond market. To borrow this money, financial institutions pledge these bonds as collateral, just like your house is the collateral for your mortgage. If interest rates rise, the value of these bonds decreases due to discounting the interest. A UK bond trader noted, ‘If there was no intervention today, yields on UK government bonds could have gone up to 7-8 per cent from 4.5 this morning, and in that situation, around 90 per cent of UK pension funds would have run out of collateral. They would have been wiped out.’

An institution might bring in £1,000,000 in equity to borrow £9,000,000 from the Bank of England at an interest rate of 1.75% and invest £10,000,000 in ten-year bonds at 3% interest, pledging the bonds as collateral for the loan. The institution could earn £142,500 per year on a £1,000,000 investment, yielding a handsome 14.25% return if market conditions remain stable. But it is a dangerous bet due to discounting. The price of a bond is its net present value. If the yield on ten-year bonds were suddenly to rise from 3 to 4%, the institution would incur a loss of £811,090, which is the difference in net present value of the bond. That would nearly wipe out the entire equity. And that happened that day.

In the past, pension funds invested in bonds for the long term, but bond yields were low. Pension funds have fixed obligations, such as paying a retiree €1,000 per month until they die. If interest rates are low, you have to pay more in pension premiums to arrive at that amount. To pump up their revenues, pension funds invested in stocks and speculated in the bond market using leverage. It seemed like easy money because central banks signal their intentions in advance. This time, however, the government took the traders by surprise, so the central bank had to rescue them.

Permanent liquidity

When there is liquidity in financial markets, you can buy or sell financial instruments like stocks and bonds at any time. In other words, you can sell them in the financial markets for currencies like the euro or the US dollar. During a financial crisis, liquidity becomes scarce, and it becomes harder to sell financial instruments. Their price collapses because there are many sellers and few buyers. Only cash and government bonds perform well in those times. Financial pundits refer to it as a flight into safety. To prevent a crisis, central banks inject liquidity into the financial system. In other words, they lower interest rates, making it attractive for investors to borrow from the central bank.